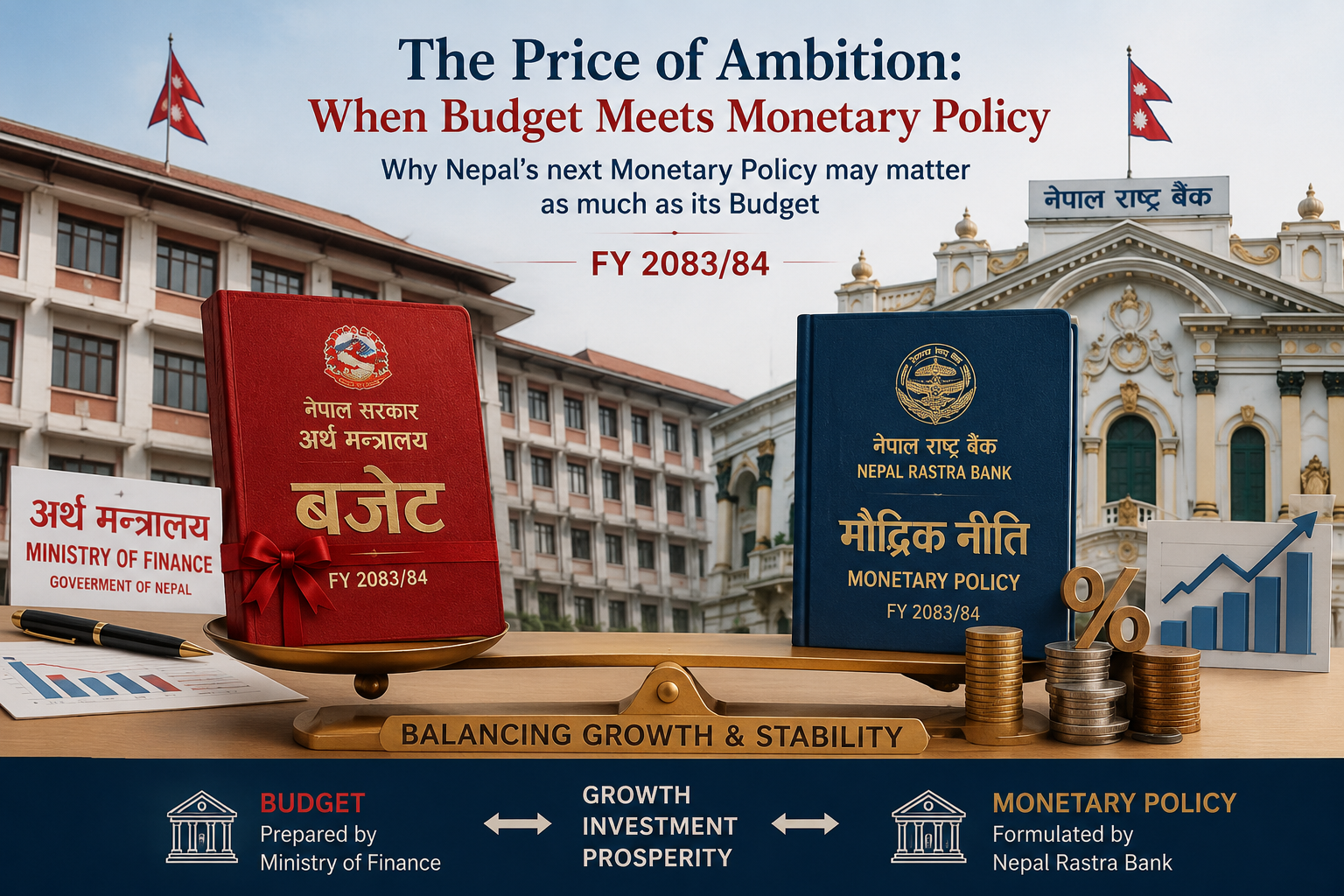

Why Nepal’s next Monetary Policy may matter as much as its Budget

Nepal’s FY 2083/84 Budget sets an unusually ambitious economic direction: lifting growth to 7 percent while keeping inflation close to 6 percent, and steering the economy toward productive sectors such as agriculture, energy and technology. Achieving this shift will require more than fiscal intent; it will require a monetary environment capable of supporting higher investment, deeper credit flows and sustained liquidity.

In practical terms, the scale of the budget’s ambition implies the need for a more accommodative—or selectively expansionary—monetary stance, particularly in sectors targeted for structural transformation. Credit conditions will need to support long-term investment, interest rates must remain stable enough to encourage borrowing, and liquidity management will have to avoid unnecessary tightening during the investment cycle.

Yet this does not mean uncontrolled expansion. The challenge for Nepal Rastra Bank lies in calibrating an expansionary bias that supports growth without breaching the inflation ceiling. In that sense, monetary policy becomes less about choosing between growth and stability, and more about managing both simultaneously.

The Budget defines ambition. Monetary policy defines affordability. The coming policy cycle will test whether Nepal can expand credit without losing price stability.

The Missing Half

Every budget tells a story, but few tell the full one. Nepal’s Budget for FY 2083/84, presented by Finance Minister Dr. Swarnim Wagle, reads like an attempt to reframe the country’s economic direction altogether. It speaks of artificial intelligence, commercial agriculture, capital market deepening and export-led growth, all under a 7 percent expansion target with inflation anchored near 6 percent.

Yet budgets, for all their ambition, do not transmit money into the economy. They do not determine whether banks lend, whether liquidity circulates, or whether credit conditions remain supportive or restrictive. That responsibility lies with monetary policy.

In practice, the central bank operates through three interconnected channels: the price of money (bank rate and policy rates), the quantity of money (liquidity management), and the direction of money (credit allocation). Together, these determine whether fiscal ambition becomes economic activity or remains a policy statement.

A Budget Written for Production

What distinguishes this year’s budget is not its size—NPR 2,124.34 billion is substantial but familiar—but its intent. The structure of spending signals a gradual shift away from consumption-led growth toward production-oriented expansion.

Energy, manufacturing, agriculture and technology are no longer peripheral themes; they are positioned as the core architecture of growth. The “Mission Mode” framing suggests an effort to move beyond incremental policymaking toward coordinated transformation.

In monetary terms, this shift implies a more demanding transmission mechanism. Credit must increasingly flow toward long-term productive investment rather than short-term consumption cycles. That, in turn, requires stable interest rate expectations and a predictable liquidity environment so that banks can extend longer-tenor financing with confidence.

Whether the budget succeeds will depend less on allocation and more on whether monetary conditions reinforce this structural pivot.

Financing the New Economy

Perhaps the most ambitious element of the budget lies in its attempt to reposition Nepal within the digital economy. Tax incentives for IT exports and the proposal for a Sovereign AI Computing Centre reflect a belief that hydropower can be transformed into digital production capacity.

Globally, low-cost renewable energy is increasingly becoming a determinant of competitiveness in computing infrastructure. Nepal’s hydropower surplus, in theory, places it within this emerging equation.

However, such transitions depend less on tax policy and more on financial intermediation. Digital firms require access to risk capital, foreign exchange convertibility and a banking system willing to evaluate intangible assets. Traditional collateral-based lending frameworks are poorly suited to this environment.

From a monetary policy perspective, the challenge is not simply to expand credit, but to adjust credit allocation mechanisms so that technology-intensive sectors are not structurally excluded from formal financing channels. In this sense, the bank rate and refinancing structure become indirect instruments of industrial policy.

Credit Before Subsidy

A similar structural shift is attempted in agriculture. The budget’s provision of a 40 percent capital subsidy for agricultural and livestock enterprises requiring at least Rs. 2 crore investment signals a move from subsistence support toward commercial scaling.

Yet subsidies operate after financing decisions are made. They reduce cost but do not solve access. The binding constraint remains the availability of long-term credit at predictable and stable rates.

Here, monetary policy plays a more foundational role. If liquidity conditions are volatile or interest rates uncertain, banks tend to prefer short-term, collateral-backed lending. That structurally disadvantages agriculture and SMEs, where cash flows are seasonal and assets are often illiquid.

The proposed First Loss Recovery mechanism attempts to address this by partially shifting risk away from lenders. If supported by monetary policy frameworks that encourage credit scoring-based lending rather than purely collateral-based assessment, it could gradually reshape financial intermediation.

The underlying logic is straightforward: subsidies may reduce cost, but credit determines whether investment occurs at all.

Markets Need Liquidity

The budget’s ambition to modernize Nepal’s capital market is unusually expansive. The introduction of derivatives, intraday trading and short selling signals an intention to move toward a more sophisticated financial system.

Yet market sophistication is ultimately constrained by liquidity depth rather than product design. Financial instruments cannot function efficiently in shallow markets.

At present, margin lending restrictions—particularly caps linked to maximum of 40% of banks core capital—act as a structural constraint on market liquidity. These safeguards serve an important stability function, but they also limit the scale of leveraged participation necessary for deeper markets.

Monetary policy, therefore, faces a balancing challenge: maintaining financial stability while ensuring sufficient liquidity for capital market development. This requires not only prudential oversight, but also clear segmentation between speculative exposure and productive financial intermediation.

Without such balance, financial innovation risks outpacing financial capacity.

Borrowing Without Crowding Out

The government’s plan to raise approximately Rs. 410 billion through domestic borrowing reflects a standard fiscal strategy. Public borrowing itself is not inherently problematic.

The issue arises when such borrowing competes with private credit demand within a constrained liquidity environment. In such conditions, government borrowing can inadvertently crowd out private investment, particularly in sectors targeted for expansion.

This is where monetary policy’s liquidity management function becomes critical. Through open market operations, reserve requirements and refinancing windows, the central bank effectively determines whether fiscal borrowing compresses or coexists with private credit expansion.

The budget’s proposed use of diaspora bonds, offshore rupee bonds and clean energy bonds is therefore significant. These instruments diversify funding sources and reduce pressure on domestic banking liquidity, easing the transmission constraint between fiscal and private investment needs.

The Digital State

Alongside production-focused reforms, the budget places strong emphasis on digitalization. The 10 percent VAT rebate on digital payments is designed to accelerate formalisation and reduce reliance on cash-based transactions.

From a monetary policy perspective, this shift matters because digital payment systems improve the transmission of policy decisions into the real economy. When transactions become traceable and instantaneous, monetary signals—such as changes in liquidity conditions—transmit more efficiently through the financial system.

However, this requires robust payment infrastructure, merchant adoption and settlement reliability. Without these, digital incentives risk remaining behavioural rather than structural.

Over time, digitalization may also enhance the central bank’s ability to interpret real-time economic activity, strengthening policy responsiveness.

Investing Tomorrow’s Reserves

One of the more forward-looking ideas in the budget is the exploration of using foreign exchange reserves through a sovereign wealth-style mechanism for strategic investments, including technology infrastructure.

Such proposals reflect a broader shift in thinking: reserves are no longer viewed solely as passive buffers, but as potential instruments of national development strategy.

However, Nepal’s external position imposes clear constraints. Foreign exchange reserves remain essential for balance of payments stability, particularly in an import-dependent economy.

Monetary policy, therefore, must carefully define the boundaries between reserve adequacy and investment utilisation. Any move toward sovereign investment structures would require strict thresholds, risk controls and institutional safeguards to prevent external vulnerability.

The challenge is not whether reserves can be used productively, but how to ensure that productivity does not come at the expense of stability.

The Grand Convergence

The central issue running through both the budget and monetary policy is not disagreement, but alignment. For much of Nepal’s recent economic history, fiscal and monetary policy have operated in parallel—coordinated in principle, but not always in transmission.

Yet the economy does not experience policy in segments. It experiences a single financial environment shaped by credit availability, liquidity conditions and confidence in stability.

A budget may define ambition. Monetary policy determines financing. Credit determines execution. Liquidity determines scale. Confidence determines sustainability.

Nepal’s 7 percent growth target is therefore not purely a fiscal objective, nor solely a monetary challenge. It is a coordination test between two policy instruments that must now operate as one system.

If that coordination succeeds, Nepal may not only meet a growth target—it may begin to reshape the structure of its economy. If it does not, even well-designed ambitions will remain constrained by financial reality.