For years, Nepal’s reinsurance market resembled a quiet kingdom with a single ruler. Nepal Re sat alone at the centre of the industry, absorbing risks from domestic insurers and enjoying the advantages that come with being the only game in town.

That era ended in 2078 BS when Himalayan Re entered the market. Competition arrived, and with it came a policy vision designed to gradually reduce Nepal Re’s privileged position. Domestic insurers were required to cede 10% of their business to Nepal Re and another 10% to Himalayan Re, but the arrangement was never meant to last. The compulsory cession was scheduled to decline by 2 percentage points each year until it eventually disappeared, allowing market forces to determine who won business.

The direction seemed clear: less protection, more competition.

Then came the Fiscal Budget of 2083/84.

In a striking policy reversal, the government abandoned the path of declining cessions and instead mandated that domestic insurers must place at least 20% of their business with Nepal Re. At the same time, reinsurance arrangements linked to the Employees Provident Fund, Citizen Investment Trust, Health Insurance Board and Social Security Fund were directed toward Nepal Re.

In effect, a company that appeared destined to compete on increasingly equal terms has suddenly regained a powerful structural advantage. The market’s former monarch has been handed a new crown. Yet this policy comeback arrives at a curious moment. Nepal Re’s latest quarterly financial statements tell a dramatically different story.

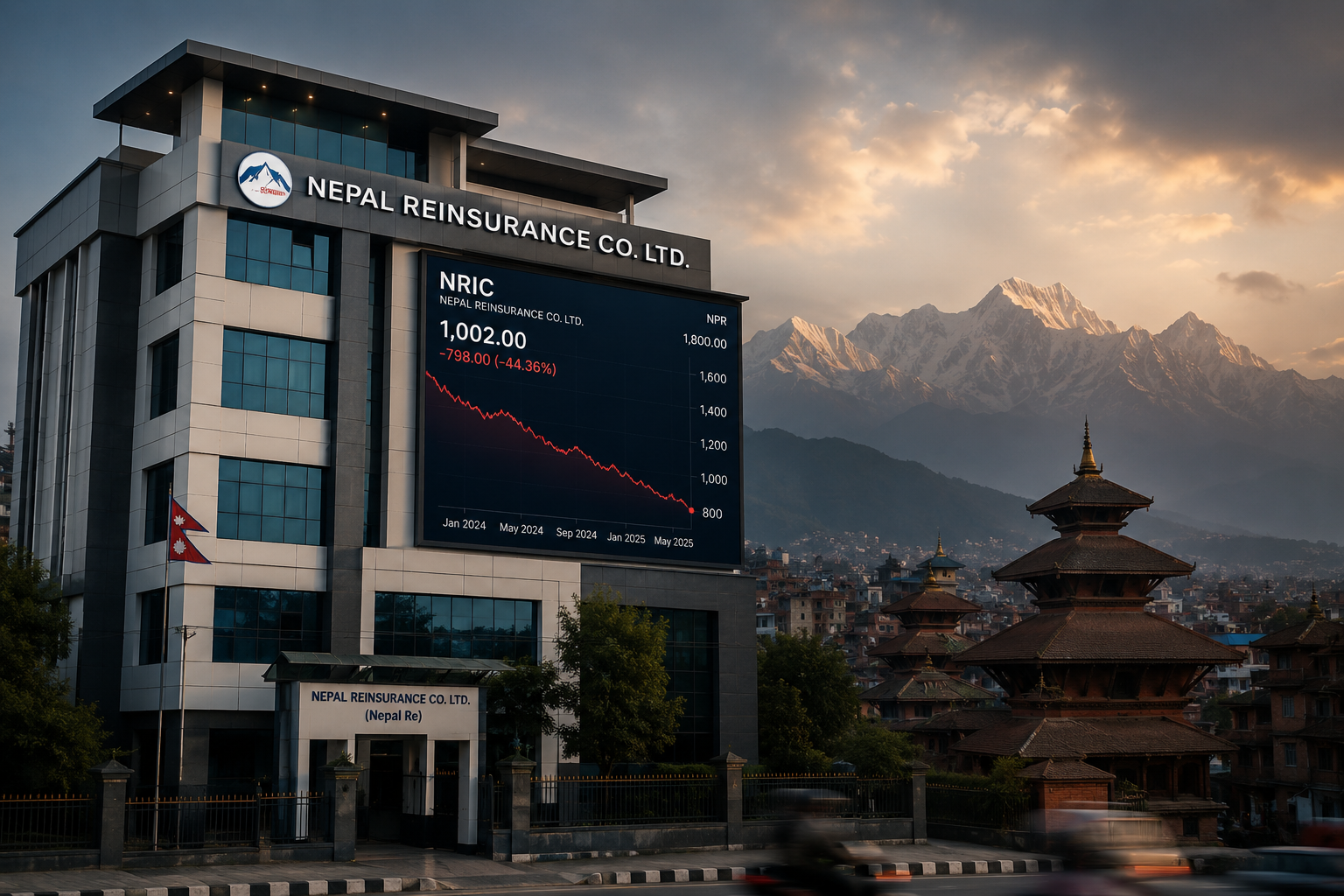

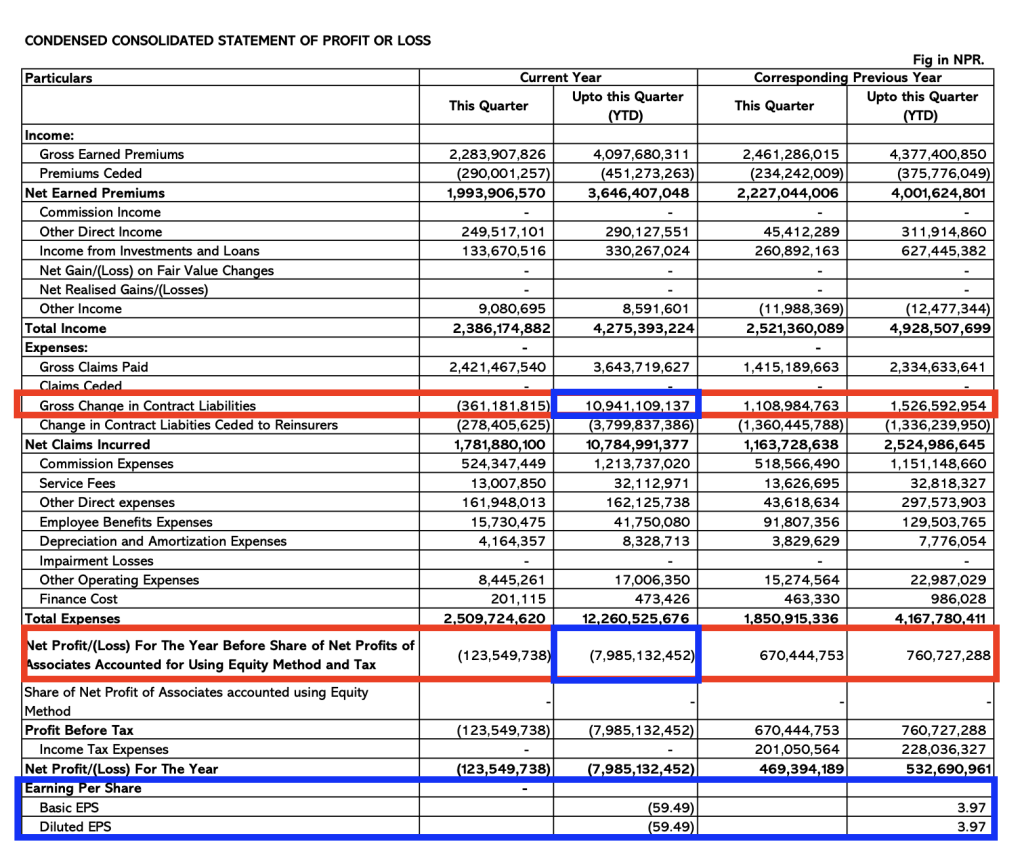

The company reported a net loss of NPR 7.98 billion for the quarter ending 31 Chaitra 2082, compared with a profit of NPR 760 million during the same period a year earlier. On the surface, the figure appears catastrophic. A loss of that magnitude would normally suggest a business in distress.

But appearances can be deceptive.

The source of the loss is not operational collapse, poor underwriting discipline or a sudden evaporation of business. Instead, it lies in a technical accounting item that rarely attracts headlines: the Gross Change in Contract Liabilities.

By the quarter ended 31 Chaitra 2082, Nepal Re’s Gross Change in Contract Liabilities had climbed to NPR 10.94 billion.

To understand why this matters, one must understand the peculiar nature of reinsurance. Unlike many businesses, reinsurers are paid today for risks that may not materialise until years later. As a result, they maintain large technical reserves to ensure future claims can be honoured.

These reserves consist primarily of two components. The first is outstanding claims, including IBNR—claims that have occurred but have not yet been reported. The second is the Unearned Premium Reserve, representing premium income received for risk coverage that has not yet expired.

When actuaries suspect that tomorrow’s claims may be larger than yesterday’s forecasts, they add to reserves. Natural catastrophes such as floods and earthquakes are familiar triggers. But social unrest can be equally disruptive. In Nepal, recent protest-related damage to property and infrastructure has underscored how quickly loss expectations can change. Faced with such uncertainty, reinsurers tend to err on the side of caution, setting aside more capital today to guard against claims tomorrow.

That increase is treated as an expense.

In Nepal Re’s case, the adjustment was enormous. The company effectively decided that substantially more money needed to be set aside for future obligations. The result was an accounting charge large enough to erase profits and produce one of the biggest quarterly losses in its history.

This naturally raises a question: if Nepal Re earned only NPR 4.27 billion in total income during the period, how can it absorb an NPR 10.94 billion increase in liabilities?

The answer lies in the balance sheet.

When reserve requirements rise beyond current earnings, the difference is absorbed through shareholders’ equity. Nepal Re’s total equity consequently declined from NPR 20.57 billion to NPR 12.50 billion.

Importantly, this does not mean the cash has disappeared.

The company still possesses substantial financial resources, including an investment portfolio worth NPR 18.84 billion and cash balances of NPR 713 million. These assets remain available to meet future claim obligations as they arise. In addition, it holds reinsurance assets and insurance receivables arising from its business with primary insurers, which represent expected recoveries and outstanding settlements rather than immediately liquid resources.

The operating ratios reveal the scale of the reserving exercise.

Net claims incurred reached NPR 10.78 billion against net earned premium of NPR 3.64 billion, producing a loss ratio of roughly 295.8%. Such a figure would ordinarily indicate severe underwriting stress. In this case, however, it largely reflects the decision to strengthen reserves aggressively.

The expense ratio stood at approximately 40.18%, incorporating commission expenses of NPR 1.21 billion alongside other operating costs. For a reinsurer that relies on primary insurers to originate business, this remains within a broadly expected range.

Combined, the two figures generated a combined ratio of about 335.98%. Any ratio above 100% signifies an underwriting loss. A ratio approaching 335% is extraordinary, though it should be interpreted in the context of the one-off liability adjustment rather than as a measure of ongoing profitability.

In the Q4 report of FY 2081/82, Nepal Re reported a loss ratio of 67% and an expense ratio of 33%, resulting in a combined ratio of approximately 100%—a level broadly consistent with breakeven underwriting conditions. This sharp contrast highlights that the current spike is driven not by a structural deterioration in core underwriting discipline, but by a significant actuarial strengthening of reserves during the quarter.

The most revealing figure lies elsewhere.

Nepal Re’s solvency ratio remains at 3.65.

For insurers and reinsurers, solvency is the statistic that ultimately matters. Regulators require a minimum ratio of 1.5. Nepal Re holds more than double that requirement and maintains assets comfortably in excess of what is needed to meet long-term obligations.

In other words, despite the alarming headline loss, the company remains financially robust.

The irony is striking. At the very moment Nepal Re reports one of its worst quarterly results, its strategic position may be stronger than it has been in years. The government’s new 20% direct cession requirement guarantees a substantial stream of premium inflows. The addition of large public-sector insurance programmes further strengthens that pipeline.

Viewed through that lens, the quarter looks less like a crisis and more like a reset.

The NPR 7.98 billion loss is undeniably significant. Yet it is primarily an accounting reflection of caution rather than weakness—a decision to recognise future risks today rather than postpone them for tomorrow.

Markets often focus on income statements because losses are dramatic and easy to understand. Balance sheets tell slower, more complicated stories. Nepal Re’s latest results suggest that while the income statement is shouting, the balance sheet is whispering something very different.

And investors would be wise to listen.

For Nepal Re, the quarter may ultimately be remembered not as the period in which profits disappeared, but as the moment the company strengthened its reserves, secured a renewed policy advantage and positioned itself for the next chapter of Nepal’s insurance market. The loss is immediate. The strategic gain may endure for years.